The 30s are a decade of settling into both your personal life and career. It is a time of challenge and responsibility, but you can handle it well if you manage your money properly:

#1 Pay off expensive debt as soon as you can. As a 30-something person, you most likely have some debt in the form of a car or home loan. Some people have credit card loans, too. This is the decade that you reconcile your savings and spends judiciously, and the first area to pare money spending is in the area of expensive debt. Make a plan to restructure your debt, and look for ways to pay off the debt as soon as you can. Being debt-free saves up a substantial portion of your income that you can use for your family’s goals. #2 Use credit cards responsibly. Almost every person in the UAE uses credit cards, but only a few are responsible with them. It is not enough to get the best platinum credit card in the UAE if you are unaware of how to use the card to your advantage. Do remember to use the bank’s credit in a way that you remain well within your monthly credit limit and pay the balance/bill before due date. Your credit utilisation ratio should be as low as possible to avoid paying interest on the card. When used correctly and responsibly, your platinum credit card can gift you a spate of rewards and experiences. Not only do the best platinum credit cards in the UAE offer a range of travel benefits, they also give reward points for shopping, insurance for travel, shopping and car rentals, concierge services and add-on cards for family members. #3 Save money every month, and even in between. It is never too early to inculcate the savings habit. A savings fund helps you on a rainy day, or pay for unexpected emergencies, or to simply plan for the future. But there is a trick to saving money that most people are unaware of: instead of waiting to save at the end of the month, set aside a portion of your income the moment you get paid. This way, you are certain of saving money instead of scraping together some money (or none at all) at the end of the month. It keeps you on course to create a sizeable savings fund for the future. Make sure you never withdraw from the account but only deposit money in it. #4 Start planning for your retirement. Your 30s are the best time to plan for your retirement. By now, you are clear about your financial goals and the age at which you can realistically retire. Set a retirement age, say 45 or 55 years, and work backwards from there. Invest in a pension scheme, buy term insurance that can be renewed or extended at maturity, and create a separate retirement savings fund. You might even consider investing in a second property to serve as your retirement house instead of maintaining your current large house post-retirement. By the time you retire, you should have a sizeable corpus waiting for you. #5 Curtail expenditure wherever possible. One of the most enduring ways to save money and create wealth is to curtail unnecessary expenditure. Take stock of your monthly expenses and cut out all the areas that you can do without. This includes curtailing shopping binges, driving more than necessary, eating out frequently, investing in expensive health memberships instead of running at the park, etc. As a greater portion of your income is now retained with these curbs, you can increase your savings allocation.

0 Comments

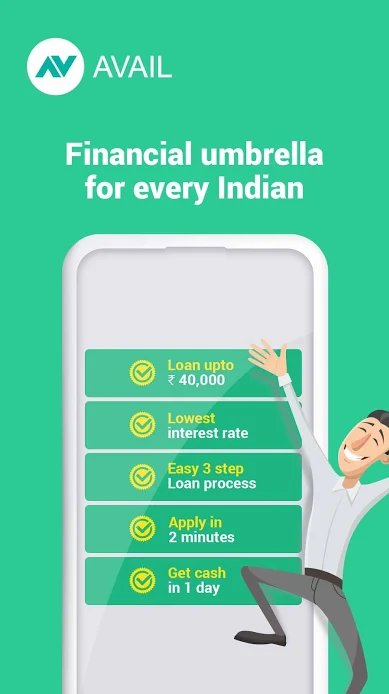

The need for extra cash can arise suddenly, leaving you with little time to prepare. During such situations, the best option can be to avail of a loan to fulfil your financial obligations. With the facility of instant loan online india, now you no longer have to visit a bank and go through a lengthy process to get your loans approved. You can download an instant loan app in india and manage your financial crunch independently.

If you are in two minds, we have rounded up the benefits of loans to help you make an informed decision. Flexible Opting for a loan from a credible lender gives you the flexibility to return the loan at your pace. Of course, there will be a term defined, and you will be required to make regular instalments to clear your loan. However, it is always better than taking the money from a friend or family. For all you know, they may have a financial crisis tomorrow and expect you to return the amount then. Smooth Application Process All you need to apply for an instant loan through an app is a smartphone and your documents. After checking your eligibility, you can proceed to fill out your application on the app. You will be required to submit a few documents like your Aadhar card copy, income proof, PAN card copy and address proof. If you have all your papers in place, applying for a loan will not take you more than a couple of minutes. Quick Disbursal When you choose to avail of an instant loan online india, you will be surprised to know the speed at which the money gets credited into your account. After the approval of your online application and KYC, the disbursal can happen within one working day. If there is a medical emergency, this amount can help you get medical aid at the right time. Reasonable Interest Rates When you apply for a loan via an instant loan app in india, the interest rates are within reach of the common public. It will not burden your pocket and will not impede your monthly budget. You will be able to sail through your current situation or buy a product that needs priority at the moment without any hassles. Transparent Processing Fee Most instant loan apps are transparent about their processing fee and other charges related to loan disbursal. You can be rest assured that you will not be caught off-guard. If you have any doubts or want to be doubly sure, you can call customer care and check. Improves Credit Score Your credit history and score are a few parameters that help banks understand your ability to return the loan amount. With a reasonable score, the possibility of getting a bigger loan or a credit card gets enhanced by many folds. With regular and consistent repayments of your loan instalments, you can improve your credit score. Pre-close Your Loan If you are self-employed and happen to make good sales in a month, you can go ahead and close your loan before the tenure. However, you may want to check if there is any penalty or processing fee for foreclosing the loans. Financial Independence Finally, loans allow you to be financially independent in the truest sense. They help you manage your financial needs without having to ask anyone else for cash. It will give you the confidence to take on bigger matters in life. Conclusion It is a myth that loans are a financial burden. On the contrary, they help you meet your financial needs independently. With instant loans at your bay, now you can avail of them from the comfort of your homes.  A lot of people are wary about using credit cards, because there are several myths associated with them. Chief among these is that they encourage reckless spending. But think about it – is reckless spending a function of a reckless spender, or a behaviour that a responsible spender might suddenly cultivate? If you are habituated to spending within your budget, paying all your bills on time and getting out of debt as soon as possible, you are a good candidate for a credit card.

Did you know that your credit card can keep your money safe? These are 4 ways in which it does: #1 You get access to a line of credit instead of finishing your account money. The fundamental difference between a credit card and a debit card, is that the former offers you access to a line of credit from a reputed bank. The latter is connected to your bank account, so any spends on it directly deduct money from your account. Whereas with a credit card, you can use the bank’s credit for free if you remain within your monthly credit limit and pay the balance/bill before due date. Thus, it is a more cost-effective and financially responsible way of spending money. #2 The best banks offer a range of offers – these save your money. Getting a credit card in Dubai is easy as pie, but not all cards are equally good. Always take a credit from a leading bank in the city, and start by checking your eligibility for the credit card. The credit card eligibility decides what kind of card the bank can give you, and the corresponding range of benefits. Usually, the higher your income and the more established your repayment ability, the better the range of rewards and experiences that the card issuer offers. If you have a higher income you can get a range of benefits on travel, concierge services, points for shopping at member outlets, eating out at certain partner establishments, and so on. These save money in the long run. #3 It helps build credit history. Credit card usage is one of the first behaviours potential lenders check when you apply for institutional funding. If you have a credit card and you use it responsibly – stay within your credit land and pay balances in full instead of carrying them over every month – it ends up adding to your credit score. This is a big plus when you seek a home or car loan in the future. #4 It protects against fraud and phishing attacks. One of the biggest advantages of using a credit card is that it keeps you safe from fraud and online theft, which a debit card cannot do. Credit cards offer greater protection, especially if they have been stolen and you report the loss within 24 hours. Doing so reduces your personal liability in the theft and you are not made to pay the amount that the thief swipes on the card. Second, the credit card is not linked to your bank account so a phisher or hacker cannot access your savings directly. If a transaction is made using your card, you can immediately stop it from processing any further ones with just one phone call to the bank. The hacker cannot steal using your credit card if they depend on its PIN; any theft can occur only if the actual card is stolen. A credit card can be a useful tool for managing your money and buying the things and experiences that you hold dear – plus, it’s safe to use! |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

August 2022

Categories |

RSS Feed

RSS Feed